In early 2021 Plymouth’s “Look II” sculpture by Sir Antony Gormley was in the headlines. Opinions on the sculpture varied, but publicity focused on its price. I welcomed new grant-funded public art to the city, but because Plymouth City Council refused to disclose the cost of the sculpture, I shared other people’s concerns about secrecy. The total cost indicated in a council budget report being £764,038.50, after deducting the cost of structural renovations – revealed following a Freedom of Information Act (FoIA) request – of £425,000, news reports suggested the sculpture cost £339,000. Mike Sheaff decided to dig deeper…

But for those of us concerned about secrecy and transparency, should its price be the main focus?

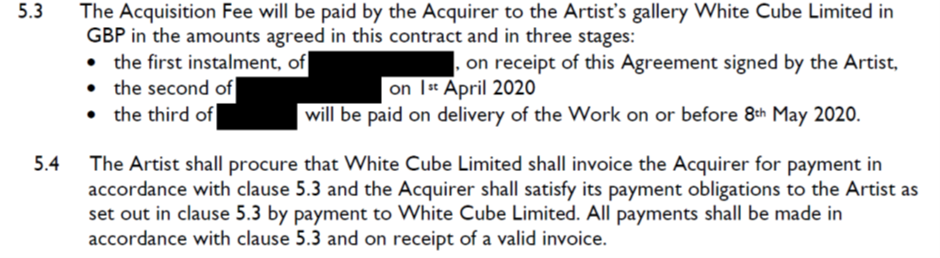

In February 2022, in response to a FoIA request I submitted in October 2020, the council eventually disclosed other sections of its contract with Sir Antony: having initially refused to make any disclosure, it had reconsidered its response following involvement by the Information Commissioner.

The contract reveals the council agreed payments would be made to White Cube Ltd:

White Cube explains in its latest accounts (to 31 March 2020) lodged with Companies House:

- as a small company it has not filed a statement of comprehensive income,

- it “has taken advantage [of exemptions in Financial Reporting regulations] to not disclose transactions with wholly owned group entities”; and

- “The immediate parent undertaking is White Cube (Jersey) Limited, a company registered in Jersey. The ultimate controlling party is JM Jopling, by virtue of his shareholding and directorship in the ultimate parent undertaking.”

This protective barrier for the company is not new. Nearly a decade ago a report in The Art Newspaper noted:

“White Cube’s businesses are complex. Records at Companies House show that the gallery’s founder, Jeremy “Jay” Jopling, is registered as the director of three entities: Mansmoor Ltd, a “consultancy and advisory” service with an annual income of £50,000; Fig-1 (2000) Ltd, an artist showcase founded more than a decade ago; and MYJ Services Ltd, which provides “services and management” to art galleries and has a turnover of around £11.8m a year […] Its most recent accounts show a series of transactions taking place between the company, Jopling as an individual, and two limited liability partnerships (LLPs), registered in Canada.”

The report’s authors comment:

“As companies including Starbucks, Amazon and Google face daily scrutiny of their UK corporation tax bills, how do commercial galleries with businesses juggle their tax payments? The answer, as ever in the art market, is clear as mud.”

There have been many calls for greater regulation of the art market, including in the Financial Times: How Transparent is the Art Market, and Can the art world clean up its act? The argument for transparency will likely be strengthened by the case of Inigo Philbrick, who in little more than a decade went from being an intern at White Cube to facing a possible twenty-year prison sentence for fraud in the United States.

Eileen Kinsella in Artnet News describes how Philbrick, having led Jopling’s secondary-market business, “capitalized on the market’s opacity”. Jopling told Kinsella, “He struck me as a smart, ambitious young man with a good eye for art and an impressive commercial sense”. Jopling gave Philbrick financial support, and Kinsella notes, “Jopling is one of numerous players jostling to be among the first in line to get his money back.” Jopling was granted an injunction in London’s High Court to protect his business interests with Philbrick, with three other offshore entities and shell companies filing similar claims:

“It appears Jopling worked with Philbrick through a mysterious offshore entity called Ogini Ltd, which was incorporated in Jersey in the Channel Islands in 2017. Although Jopling declined to comment on whether he owns the entity, the address for Ogini is identical to a White Cube entity also registered in Jersey, and Jopling previously disclosed that the court granted his injunction request on November 1, 2019 – the same date as an injunction granted to Ogini. A source familiar with the filing says it contains exceptionally detailed information on Philbrick’s activities, suggesting a close relationship between the entity and the dealer. Another clue? Ogini is Inigo spelled backwards”.

On 18 November 2021, as reported in The Art Newspaper, Philbrick pleaded guilty to fraud. When asked by the judge why he did it, he answered, “I did it for money, your honour”. With sentencing due on 18 March 2022, his attorney commented:

“The industry is corrupt from top to bottom. Inigo isn’t the cause here, he’s a symptom. I suspect many more cases like this would appear if the art world were investigated thoroughly.”

Whether or not this is true, the secrecy shrouding the art market is the problem. Reviewing the episode, two US Professors of Sociology observed:

“Philbrick’s case is instructive not because it is the most extreme, but because some of his tactics – like the use of offshore entities and shell corporations in art-financing deals – are still widely exercised in the art market […] The Philbrick affair has something to teach us about the governance of the art market, the ways we form trust in systems, and the ways we might reform this one.”

Plymouth City Council’s justification for continuing redactions suggests we have some way to go:

“Clauses 1.2, 2.3, 3.2, 4.2, 4.4, 6.2 and 7.0 contain specific terms resulting from those negotiations, which, if placed in the public domain, would potentially be available to other possible future clients of the artist. These terms contain information that would provide other potential clients unfair leverage prejudicing Sir Antony’s ability to effectively negotiate similar provisions in future contracts, thereby undermining his commercial position in the art market.”

Individual local authorities have little power to challenge the art market’s opacity. Commercial interests may legitimise secrecy on price, but if public money is channelled through companies hidden from public view, this should surely be open to scrutiny.