As NHS watchers are only too aware, there’s constant wrangling over NHS finances: it’s a bottomless pit; it’s mismanaged; it’s a huge amount; it’s not enough; will never be enough….Where to start with all of this? Let’s take a look...

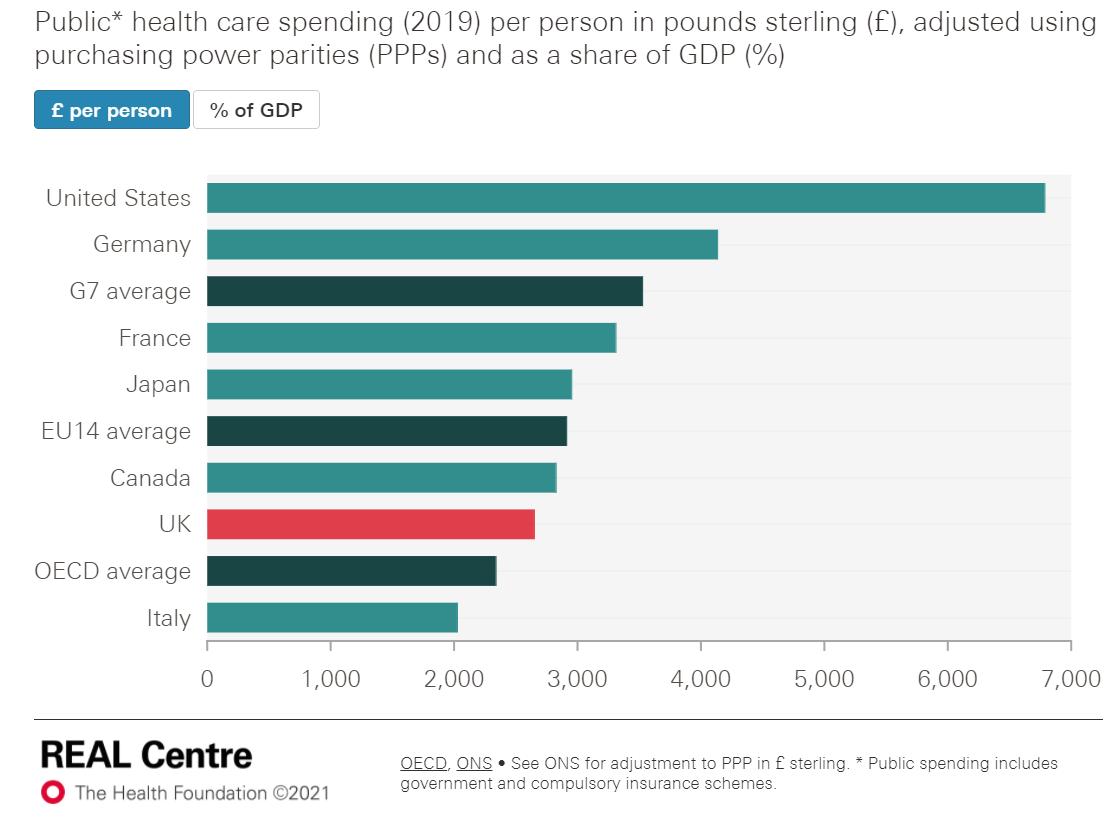

Does the UK spend on healthcare match that of comparable countries?

Well, no. Neither as a proportion of national income nor per head of population. The UK spends less than average. In comparison to G7 countries, the UK’s spend was second lowest:

So, yes, the UK does spend a huge amount on healthcare; however, it’s no more and in fact less than comparable countries

Fact 1: In order to have good healthcare we have to pay for it

Has UK spend on the NHS changed over time?

Yes:

Until the financial crash of 2008, the NHS had received an annual uplift of approx 3.7 per cent since its inception.

After 2008, this was reduced to 1.4 per cent and has stayed at this level up to 2019

Fact 2: Spending on the NHS has reduced in real terms since 2008

What does the money go on?

Well, essentially salaries, medicines, equipment, buildings….

Interestingly, we have markedly fewer qualified staff: fewer doctors, nurses, and allied health professionals such as physios.

We now have 2.6 doctors per 1000 compared to 3.6 per 1000 in 2010 (when the Conservatives came back into power)

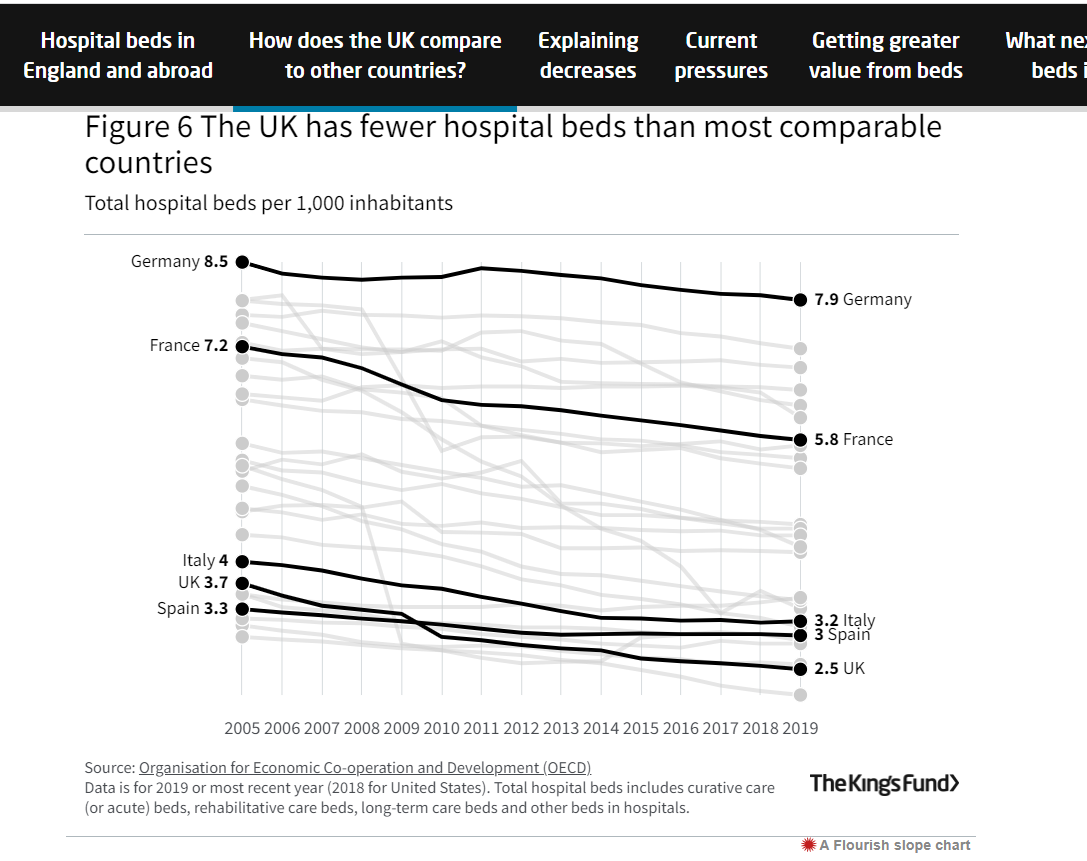

We have fewer hospital beds. Since 2010 we have lost 16,000 beds, including over 5000 acute and 6000 mental health beds. In 2019/2020 (the last available figures) we had 2.6 beds per 1000 compared to 4.5 per 1000 average

Fact 3: We have fewer qualified staff and fewer beds from our funding

How much of the NHS budget goes to private providers?

The proportion of total funding spent on private providers is approximately 26 per cent. [The government claim 7 per cent, but here is an explanation of the discrepancy from Patients4NHS:

In 2019, the Department of Health and Social Care (DHSC) claimed that spending on clinical services with “independent sector providers” has accounted for just over 7% of its budget, and that this has been the case for the previous five years. In contrast, analysis by the Centre for Health and Public Interest (CHPI) found that major items of expenditure on the private sector are excluded from DHSC’s calculations and that the figure is actually 26%.

The difference arises from using different figures for the analysis. The CHPI analysis uses figures from NHS England rather than from the DHSC. It includes spending not considered by DHSC, such as spending on GP services as well as other primary care services, such as those provided by pharmacists (e.g. Boots) and opticians (e.g. SpecSavers), and payments to local authorities (e.g. for nursing and social care services), as most of these payments end up in the independent sector.

The discrepancy also arises from different understandings of ‘the independent sector’ and whether there is a clear distinction between this and other sectors, such as ‘the voluntary sector’, ‘local authorities’ and ‘the private sector’. ]

In short, it is not transparent but hidden, according to CHPI’s 6 year review.

This lack of transparency makes it impossible to understand if this outsourcing represents value for money and where money in system is actually going: into services or into profit?

One in three NHS-funded knee replacements now take place in private hospitals and almost one in five hip replacements according to the Royal College of Surgeons, as do 27 per cent of hernia repairs and 20 per cent of cataract procedures. This compares with almost none in the mid 2000’s.

What changed?

The 2012 Lansley reforms accelerated private provision.

Lansley opened the door for provision of private services such as GP surgeries, out of hours services, urgent care and minor injury units, diagnostics, maternity care, elective surgery, community nursing,ambulance services, prison health, wheelchair services and more… private provision even extended to the running of whole hospitals.

As Professor Roy Robertson wrote to the Guardian on 20 July 2020:

The 2012 reforms were a deliberate commercialisation and marketisation of the NHS, establishing commissioning groups to allow and encourage competition and drive down costs.

Guardian

Fact 4: It’s not possible to fully understand health care spending unless transparency around private provider input is provided.

UK healthcare spending to date has not been marred by conflicts of interest….or has it?

For example: is it in the interest of the patient or the provider to order tests, referral, intervention? Do more tests,referrals and interventions equal more profit? [It is worth reading CHPI director David Rowland’s BMJ opinion piece on conflict of interest, including observations on Centene, a US healthcare provider who have got involved in primary and secondary care – aka the profit chain. Ed]

Make no mistake, this is US-style healthcare and it’s potentially happening right here, right now.

Fact 5: Significant funding allocations to private providers are taking place under the banner of the NHS logo, enabling government to maintain the illusion of a commitment to the NHS

So back to the original questions:

UK spends no more but, in fact, less than comparable countries

Lack of transparency on this spend makes it difficult to evaluate value for money.

Major transparency issues around private provider contracts now making up 26 per cent of the total health and social care budget.

So is it a bottomless pit? Not on this data.

Enough resource? Not on this data

Mismanaged? Difficult to know.

Which private providers are getting the money and for what?

How much profit is now being made that might have otherwise been used for patient care?

The current version of the health and social care bill is currently at the report stage, having passed its first reading.

Want to find out more?